Equinix acquisition of 29 data centers and their operations from Verizon Communications illustrates one issue with tier-one service provider efforts to move up the value chain. Large entities need large opportunities to “move the needle” on revenue.

Those facilities generate annual revenue in the $450 million range, too small a number to materially affect Verizon’s annual revenue of about $126 billion. In other words, the data center business represents only about three-tenths of one percent of total yearly revenues.

The point is that the revenue stream, for Verizon, is too small to matter.

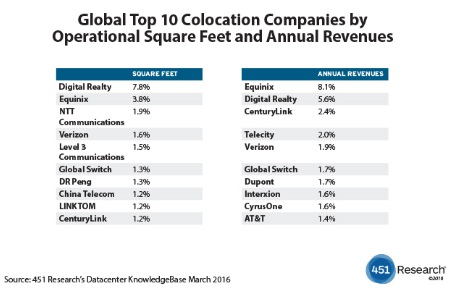

Though 451 Research projects the global colocation market will reach $33 billion by 2018, the market is highly fragmented. In 2016, for example, Verizon had less than two percent market share.

“The majority of this revenue (54.6 percent) continues to be derived from local providers with sub-$500 million in annualized colocation revenues,” analysts at 451 Research said of 2015 revenues.

As often is the case in the telecommunications business, scale matters. The colocation business simply lacks the scale attractive to most tier-one service providers. And that means the business will be dominated by specialist providers.

Another angle is that, even if large telcos tend to grow more by acquisition than organic growth, few of the “move up the stack” moves have really reached enough scale to matter, AT&T being among the salient exceptions to the rule. AT&T’s acquisition of DirecTV has, at least for the moment, dramatically affected the firm’s revenue profile.

AT&T now is the largest U.S. linear video subscription provider, and generates about a quarter of total revenue from video entertainment services. Verizon, on the other hand, earns 68 percent of total revenues from mobility.

The point is that large tier-one service providers not only must “move up the value stack,” but also need scale when doing so. Colocation, as opposed to cloud computing, remains a fragmented business. Cloud computing infrastructure is very much a winner-take-all business.

Oddly enough, both those facts--fragmentation and winner-take-all--have key implications for tier-one providers of any size. Fragmented markets are not going to make a difference. Winner-take-all markets can move the needle, but only if the telco is among the top few providers in the market.

No comments:

Post a Comment