Rural internet access, like rural telecommunications generally, always has been an economic challenge. Infrastructure costs, relative to higher-density urban areas, are higher to much higher.

The number of potential customers is far lower and propensity to spend tends to be lower as well. That is why telecom policy makers always have subsidized rural communications from profits earned elsewhere in the ecosystem (taxes and fees levied on business and urban customers).

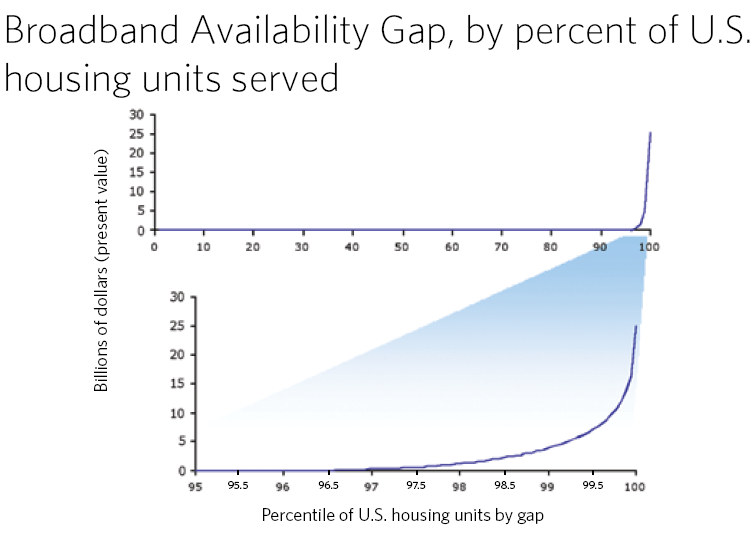

In the U.S. market, for example, the last five percent of residences is where the problem lies, with most of the cost issues related to connecting the last couple of percent of locations, as shown by the U.S. Federal Communications Commission National Broadband Plan and Broadband Availability Gap analysis.

In that regard, several major changes have happened since the end of the monopoly era. For starters, the high profits once earned from business customers have diminished sharply. That matters because it was those profits that funded the money-losing networks in rural areas.

A rough rule of thumb always has been that mass market telecom providers make money in urban areas, break even in suburban areas and lose money in rural areas.

That is not likely to change, though the magnitude of losses in rural areas, and the breakeven situation in suburban areas, are the subject of much activity (switching from fixed to wireless or mobile access, for example).

To be sustainable on a stand-alone basis, rural networks have to rely both on better technology that is much more affordable, and always must keep operating costs in control. The former tends to be the issue. Rural companies always have had to operate efficiently.

Government subsidies likely always will be needed, as an actual sustainable business model does not really exist.

Consider many U.S. states where rural population density ranges between 50 and 60 locations per square mile, and ignore the vast western regions east of the Pacific coast range and west of the Mississippi River, where population density can easily range in the low single digits per square mile.

Assume 55 locations per square mile, and two fixed network suppliers in each area. That means a theoretical maximum of 27 customers per square mile, if buying is at 100 percent. Assume for the moment that buying rates really are at 100 percent. Two equally skilled competitors might expect to split the market, so each provider, theoretically, gets 27 accounts per square mile.

At average revenue of perhaps $75 a month, that means total revenue of about $2025 a month, per square mile, or $24,300 per year, for all the customers in a square mile.

The network reaching all homes in that square mile might cost an average of $23,500 per home, or about $1.3 million.

At 50 percent adoption, that works out to roughly $47,000 per account in a square mile, against revenue of $900 per account, per year. Over 10 years, revenue per account amounts to $9,000.

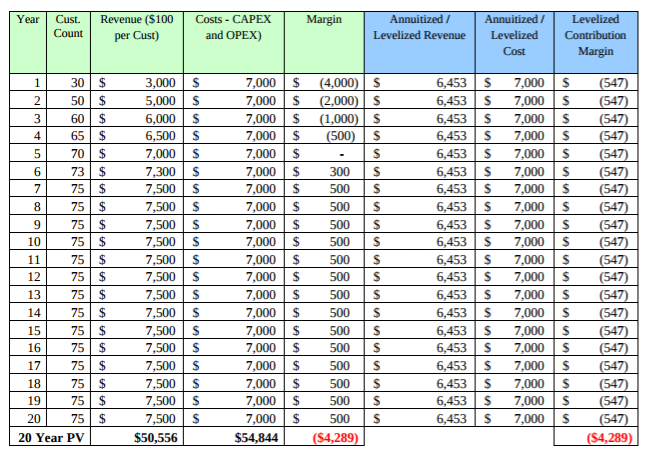

The business case does not exist, without subsidies.

Other Federal Communications Commission studies also suggest the business case challenges. Assuming a standard fixed network investment cost, that might not produce a positive business case over a 20-year period, the FCC has suggested.

No comments:

Post a Comment