One obvious fact about the competitive telecom business that makes it quite different from the old monopoly business (pre-1990s) is that better technology often has its greatest impact in the areas of operating cost or asset efficiency, even if the advantages are said to include ability to offer new services.

Although new technology more frequently reduce some forms of capital investment, new platforms sometimes drive big new revenue opportunities. Signaling system 7 improved telco operations, but also created the ability to offer text messaging as a retail service.

Optical fiber access networks add enough bandwidth that telcos could offer video entertainment services.

With a few exceptions, though, new platforms in the internet era have had very mixed implications for service revenues. The main problem is simply that the newer platforms (with the exception of enabling video entertainment), do not necessarily represent a chance to grow legacy revenues. Instead, new platforms mostly enable different (and arguably better) ways to deliver current services. The point is that, on a net basis, the better platforms do not necessarily represent “new” revenues, just better ways to supply “old” functions.

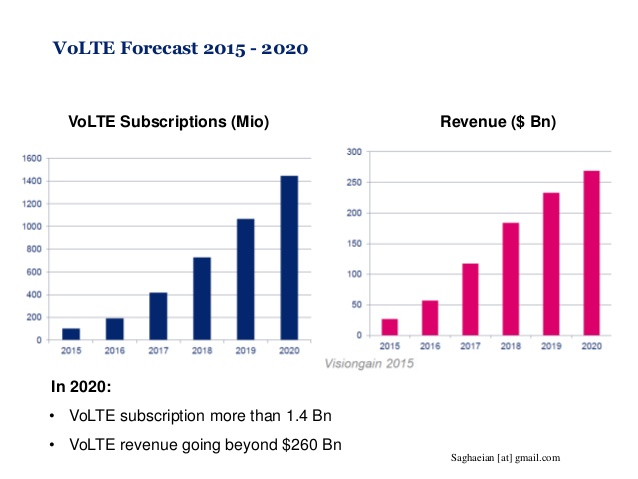

Consider voice over LTE (VoLTE). There are now 165 operators in 73 countries investing in VoLTE, including 102 operators that have commercially launched an high definition voice service using VoLTE in 54 countries, according to Juniper Research.

Some might interpret that development as representing a new revenue stream, in the form of high-definition voice services that are sold at a different price point. It remains to be seen if that actually happens. Some might argue HD voice only makes mobile voice usable where it frequently now is very sub-par in terms of audio quality.

In other words, mobile voice is “broken” and HD voice just fixes the problem, making mobile voice usable.

Likewise, some argue that over the top voice represents a revenue opportunity for mobile service or fixed service providers. The same might be said for voice over Wi-Fi. In most cases, though, such OTT voice mechanisms mostly provide indirect business value, operating cost savings or more-efficient use of existing assets.

For example, VoLTE means operators can avoid using 3G for voice services, freeing up capacity for other purposes, plus allowing simpler operations. Voice over Wi-Fi allows mobile operators to offload voice access operations in a more seamless way.

Still, for the most part, new platforms do not represent a net gain in service revenues. Part of the reason is simply that VoLTE replaces 3G voice, for example. To some extent, even investments in FTTH only allow telcos to keep pace with other competitors who are driving higher speeds, though FTTH does make high-quality entertainment video possible for a telco.

But since many alternatives exist for every legacy product, OTT voice and messaging allow new competitors to offer those services, with some ability to add features to a carrier service. That has a net negative impact on carrier revenue potential.

The larger point is that, in a competitive market, even better access platforms do not necessarily represent a huge net gain--if any--in carrier capabilities, where it comes to providing new services.

No comments:

Post a Comment