SoftBank CEO Maysaoshi Son argues Sprint must be allowed to purchase T-Mobile US in order to have a shot at massively disrupting U.S. mobile markets.

U.S. regulators are reluctant to allow the number of leading U.S. mobile operators to shrink from four to three.

European regulators face the same issue in France, for example. Operators believe consolidation has to happen, while regulators fear the consequences of reducing the number of service providers from four to three.

SoftBank’s own experience in the Japanese market would suggest Son is correct. When SoftBank purchased the Vodafone assets in Japan in 2006, that operation was the number-three provider, as is Sprint in the U.S. market.

All observers agree SoftBank rather quickly took significant new market share, largely by attracting a larger share of customers than its competitors.

Vodafone’s Japan mobile assets, when purchased by SoftBank, had market share of about 17 percent. On the other hand, Vodafone’s business had fallen from a high of about 19 percent market share in 2003.

Today, SoftBank has about 20 percent share of market.

So, In other words, the net swing in market share since 2006 (eight years) has been about three points, though only one percentage point from the 2003 high.

Granted, SoftBank is growing at the expense of KDDI and NTT. But that is a rather long, slow grind, not a whipsaw and dramatic share shift. And SoftBank remains some distance away from number-two KDDI, which has 28 percent share, while NTT Docomo has 50 percent market share.

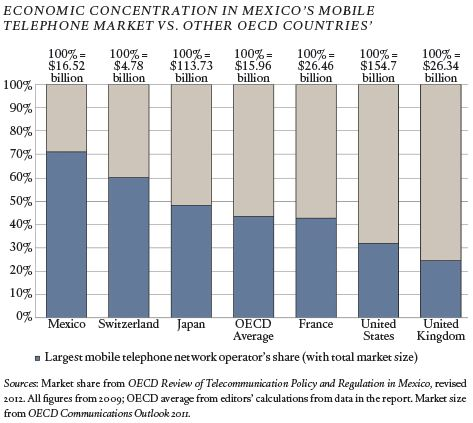

Some would argue that, globally, most mobile markets feature rather extreme concentration of market share by two providers. A share of between 25 percent and 70 percent would be within the range of expectations, with share in excess of 40 percent held by the number-one provider in Organization for Economic Cooperation and Development countries.

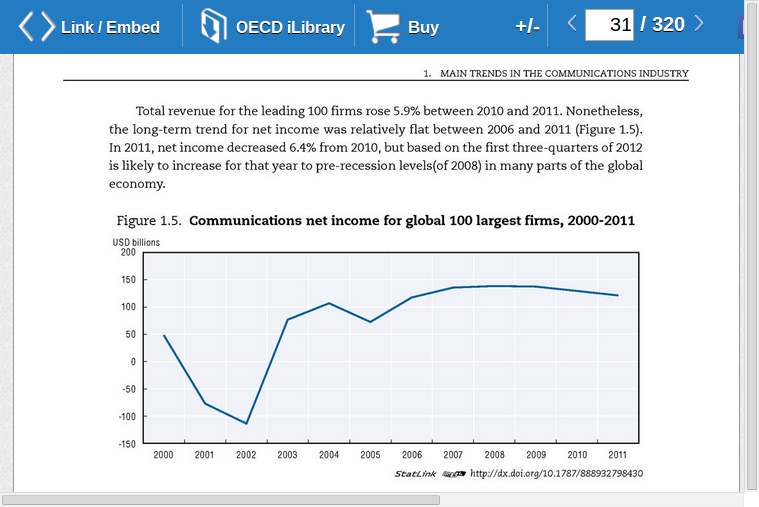

Others would point to flat revenue growth for tier-one service providers globally, though there are exceptions. Since about 2007, revenue for the top-100 firms globally has been “stagnant” to “declining.”

There are clear implications, namely the growing need for scale to offset declining gross revenue and profit margins in a growing number of markets.

“We need a certain scale, but once we have enough scale to have a level fight, OK. It’s a three-heavyweight fight. If I can have a real fight, I go in more massive price war, a technology war,” Son said on the Charlie Rose TV show.

Without T-Mobile US assets, Sprint cannot rapidly and massively challenge either firm, Son has said. That is partly a view based on SoftBank’s experience in Japan.

SoftBank’s own history in the Japanese market, and the recent experience of Illiad’s Free Mobile in France, might suggest that even a fearsome attack by a number-three or number-four service provider can succeed only to a certain extent.

No comments:

Post a Comment