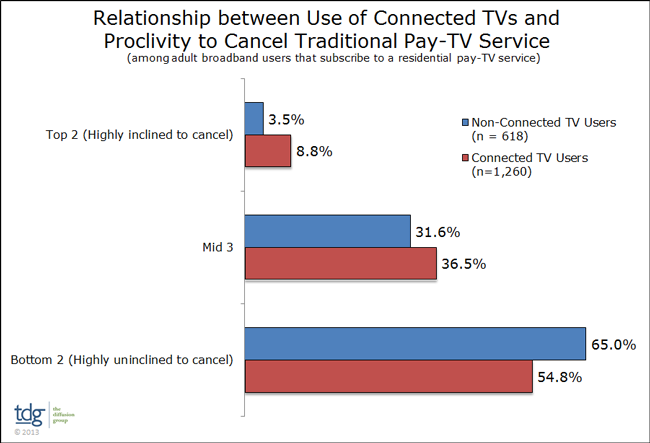

Adult broadband users with an Internet-connected TV are twice as likely as those with non-net-connected TVs to be “highly inclined” to cancel their current subscription video service, according to a new report from The Diffusion Group (TDG Research).

Those findings likely would not come as a surprise to anybody who normally watches developments in the video entertainment business. It is a trusim that a person cannot become a user or customer of any product unless that person is physically able to purchase or use.

So it should not be a great surprise that when able to view Internet-delivered TV on a big screen TV, some users might decide they can do without a video subscription. Without the ability to view Internet-delivered video, a person has no option to consider whether that experience is a reasonably workable substitute for a video subscription.

To be sure, most people probably would simply augment what they already do, and add some Internet sourced TV to their broadcast TV or video subscription or other home video sources such as Blu-ray players.

But perhaps seven percent of consumers, at any given time, might be interested in abandoning their video subscriptions for some sort of over the top or broadcast TV alternative, TDG Research suggests.

Some 8.8 percent of connected TV users say they are highly inclined to cancel their current subscription TV service in the next six months, compared with only 3.5 percent of non-net-connected TV users, TDG Research says.

Virtually no executives whose firms are major providers of subscription video services would argue it makes no difference to their revenues were widespread abandonment of subscription TV to be replaced by widespread viewing of over the top alternatives.

On the other hand, assuming they are not forced to offer low-cost “unlimited” service where there is no matching of usage to retail price, watching more over the top television is going to create demand for orders of magnitude more bandwidth.

So yes, service providers will lost a big chunk of video revenue. But they will gain a big chunk of Internet access revenue. Or so the logic might suggest.

The stumbling block, and it is a serious problem, is a shift of rival major competitors to something like Google Fiber’s pricing and usage plans: unlimited usage of a 1 Gbps symmetrical Internet access service, for $70 a month.

That would wreck most tier-one service provider revenue models, in the event of a major drop in video subscriptions, and an equally big shift to over the top services using Internet delivery.

There is one more huge issue as well. In addition to spending more for Internet access, consumers will still be paying for the TV programs or channels they want. When all the costs are added up, it is not entirely clear that the total cost of ownership will be dramatically less than what they already pay.

The conventional wisdom is that cable companies and telcos will be savaged on the revenue front when a widespread shift to over the top delivery begins. That isn’t necessarily the case.

Much depends on consumer demand. Heavier video entertainment users might find it costs less to keep buying linear TV services. Moderate users might find net costs roughly the same. Lighter users, though, probably would be best positioned to achieve savings.

No comments:

Post a Comment